From shock election results to changes in commodity prices and stubborn politicians, even seemingly insignificant events that are well beyond your control can skyrocket exchange rates or send them tumbling.

Which is why, if you trade internationally, it’s crucial to hedge in order to protect your business from the risk of fluctuations.

In the first of a series on the importance of hedging, we’re going to have a look at 9 of the biggest FX movements in history and their consequences for businesses and the global economy. Strap in. It’s going to be a wild ride.

1. The Pound Sterling’s Brexit hangover

The UK and the EU are the Ross and Rachel of international politics. Minus the happy ending.

The relationship has always been somewhat turbulent. France even vetoed the UK’s membership bid twice, in 1963 and 1967.

Things came to a head on 23 June 2016, when the UK voted to leave the EU by the narrowest of margins despite ‘remain’ having had the edge in most of the polls leading up to the vote.

Within minutes of the result, the pound shed 10% of its value — the biggest drop since 1985. But the ensuing political turmoil made matters worse. Over the next few years, the Pound would regain some stability only to plunge again with every new twist in the saga.

The situation has left businesses that export to the UK in a world of pain. By November 2016, the Pound had lost 19% of its value against the Euro, which wiped many EU farmers’ profit margins. Five Irish mushroom farms went out of business, and other producers soon followed.

2. Black Wednesday: George Soros fights the Pound and wins

The vote for Brexit may have come as a shock to some, but the writing was on the wall as early as September 1992, when the UK left the ERM. ERM stands for Exchange Rate Mechanism. It’s the precursor of ERM II, the mechanism that keeps the exchange rates between the Euro and other EU currencies stable and helps EU members prepare to join the Euro. But let’s back up for a second.

Exchange rates can be fixed or floating. Floating exchange rates fluctuate in value depending on market forces. Put very simply, if a currency is in demand, its value goes up. And if it isn’t, its value goes down. By contrast, fixed exchange rates are kept within a predetermined range or at a certain level through government intervention. The ERM was sort of in between. The Pound’s value was tied to that of the Deutsche Mark — Germany’s currency at the time. The UK government also committed itself to intervene if the market tried to push the Pound to Deutsche Mark exchange rate below a certain level.

So what went wrong? When the UK joined ERM in 1990, it was going through an economic boom. But by 1992 the tide had turned and the economy tanked. This made the Pound less attractive, so the government had to keep raising the interest rate and using its foreign currency reserves to buy Pounds to prevent the Pound to Deutsche Mark exchange rate from falling below the agreed level.

To cut a long story short, the government eventually ran out of road. Speculators — most famously George Soros — bet on the Pound being doomed. The government had depleted its foreign currency reserves, so it could no longer intervene. There was hope that Germany would swoop in. But it had problems of its own, so it didn’t. This left the UK with no option but to leave the ERM.

On the day the decision was announced — Black Wednesday — Soros reportedly made over $1 billion. Meanwhile, the Pound lost about 20% of its value. And prices shot up, eating into importers’ profits and into consumers’ disposable income.

But perhaps the biggest consequence was that the UK would opt not join the Euro. Instead, the country took a path that would lead it out of the EU 24 years later.

3. The Swiss Franc goes it alone

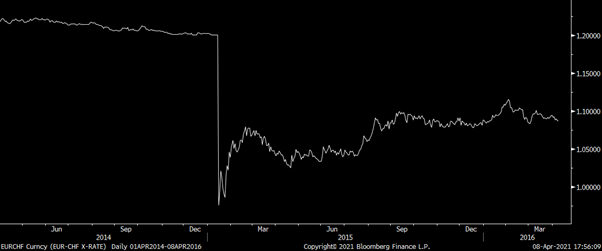

‘Unpredictable’ is the last word anyone would use to describe Switzerland. For centuries, it’s been a beacon of stability. So the markets were stunned when the Swiss National Bank announced it would unpeg the Swiss Franc from the Euro in 2015. And they were even more stunned it happened just three days after the Swiss National Bank’s vice president said the peg was ‘the cornerstone of our monetary policy’.

So what happened? First things first, here’s a brief explanation of what a peg is. In foreign exchange, pegging means fixing a currency’s value to that of another currency. In Switzerland’s case, a floor was placed where €1 couldn’t be worth more than CHF1.20. The decision to peg the Swiss Franc to the Euro came about in 2011 as a result of the 2008 financial crisis.

The financial crisis hit EU economies, most notably Greece, very hard, which made the Euro unattractive to investors. Switzerland’s economy was also affected, but not as badly as everyone thought. It also bounced back more quickly. So the markets decided the Swiss Franc was safer than the Euro. This made the Swiss Franc’s value shoot up, while the Euro’s value declined.

The Franc’s increase in value created two problems. Firstly, exports, which are very important for the Swiss economy, suddenly became a lot more expensive, especially for countries that used the Euro. Secondly, the price of imported goods went down, which put the Swiss economy at risk of deflation — a fall in the cost of living.

Long-term deflation discourages customers from spending. Instead, they keep waiting for prices to drop further. This creates a vicious cycle. Nobody buys, so nobody sells. Everyone makes less money, and the economy takes a hit.

That’s where the peg came in. With a floor under the exchange rate, European buyers would know the maximum Swiss goods would cost. This protected Swiss exports and also helped prevent deflation. Unfortunately, the Euro’s value continued to decline, so the Swiss had to keep printing Francs and buying Euro to maintain the exchange rate.

This worked for a while. Then, in 2014, the European Central Bank decided to print money too, which would’ve forced Switzerland to print even more money. Experts speculate that the Swiss government must’ve decided they couldn’t keep doing this. With the peg removed, the value of the Euro dropped 30% against Swiss Franc (see graphic), and the dollar also dropped 25% against the Franc — terrible news for exporters.

The Swiss National Bank would eventually have to intervene again and buy up foreign currency to stabilise the exchange rate.

4. The 1997 Asian currency crisis

In the early 90s, the US economy wasn’t doing well and the Dollar was weak. So many east Asian countries — these included Thailand, Malaysia, Indonesia, Singapore, and the Philippines — pegged their currencies to the Dollar to keep their exchange rates low and give their exporters a competitive advantage.

The pegs also made borrowing from foreign companies cheaper and easier. So both the private and public sectors in these countries embarked on huge, sometimes ill-advised projects on credit. Unfortunately for them, by the mid-90s the US economy started improving and the value of the Dollar increased. Because they were pegged to the Dollar, the value of these countries’ currencies also went up.

Exporters were hit hard and investment dried up. Worse, speculators started betting against these currencies on forex markets, which forced governments to intervene to maintain their pegs.

In July 1997, Thailand ran out of foreign currency reserves and had to ditch their peg. Their currency, the Baht, collapsed. The Indonesian Rupiah, the Filipino Peso, the Singaporean Dollar, and the South Korean Won followed soon after. All in all, east Asian countries’ currencies collectively lost about 38% of their value. And the International Monetary Fund had to step in to help.

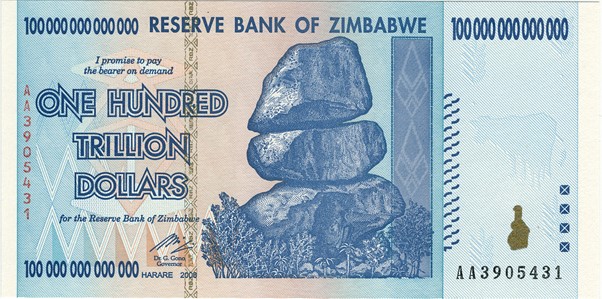

5. The Zimbabwean Dollar’s collapse

Can you imagine doing business with a country whose currency halves in value every single day? Between 2007 and 2009, this was the reality in Zimbabwe.

A combination of high government debt, a weak economy, and ill-advised policies led to hyperinflation — an uncontrolled, continually worsening rise in the cost of living. Once the momentum started, it was impossible to make it stop. Things got so bad that the Zimbabwean Dollar started losing value simply because people expected it to do so.

At its peak in 2008, inflation was increasing by 79.6 billion percent every month — that’s 796 and eight zeroes. The Reserve Bank of Zimbabwe was printing one hundred trillion dollar bills that would become worthless in a matter of days.

In April 2009, the government gave up and started using other currencies, primarily the US Dollar. The US Dollar remains the preferred currency to this day, despite attempts to revive the Zimbabwean Dollar’s fortunes.

6. The Venezuelan Bolivar gets itself in hot oil

You know it’s really bad when it makes more sense to use banknotes to wipe than pay for actual toilet paper. That’s exactly the situation Venezuela’s currency, the Bolivar, found itself in in 2018 due to hyperinflation. The Bolivar’s woes started when the price of oil crashed in 2016. This happened because the supply of oil far exceeded demand.

Oil makes up a whopping 99% of Venezuela’s export revenues. So this was bad. Once people stopped buying Venezuela’s oil, they didn’t need Bolivars, either. As a result, the Bolivar’s value decreased, imported goods — including staples like food — became more expensive, and the government started having trouble paying its debts. The government’s solution was to print more money. This can make sense. But only as a short-term fix.

Unfortunately, the oil markets just wouldn’t bounce back, so the government’s approach made everything worse. Because the supply of money increased and demand for it didn’t pick up, its value decreased. By July 2018, prices had risen by 82,700% and the Bolivar had lost over 90% of its value. To put that in perspective, merchants had trouble printing till receipts because there wasn’t enough space on them to fit all the zeroes.

The Bolivar was discontinued in August 2018 and replaced by a new currency called the Bolivar Soberano. But things are bad to this day. Between 2020 and 2021, the price of a cup of coffee rose from 100,000 new Bolivars to 3,403,620 new Bolivars — a 3,304% increase.

7. The US Dollar meets its match

Because Canada and the US are close neighbours with interdependent economies, the Canadian Dollar and the US Dollar have always moved hand in hand. But, in 2007, the Canadian Dollar’s value rose by 50% and briefly reached parity. In other words, C$1 was worth $1. At the time, the price of oil had reached an all-time high due to growing demand.

Canada has the largest oil reserves in the world, and the US buys 98% of its production. This meant more US Dollars were being exchanged for Canadian Dollars, which increased the latter’s value.

The Canadian Dollar’s rise had huge implications for US-Canada trading relationships. The Canadian Dollar’s rise was good news for US exporters because it made their goods cheaper. On the flipside, raw materials imported from Canada became more expensive.

8. Two become Yuan

In 1994, China had two exchange rates. There was the official exchange rate, managed by the Chinese government. And there was an ‘unofficial’ (read, black market) exchange rate, which was much lower.

To maintain the official exchange rate, the Chinese government had to intervene in all sorts of ways, including placing restrictions that were hurting the country’s economy. At the same time, the vast majority of commercial transactions — around 80% — were already taking place using the ‘unofficial’ rate.

So the Chinese government decided to ditch its ‘official’ exchange rate and peg its currency, the Yuan, to the US Dollar at the ‘unofficial’ rate. Because the unofficial Yuan to US Dollar exchange rate was much less favourable to the Yuan than the ‘official’ rate, it’s often thought that the Chinese government devalued the Yuan. But in fact, all the government did was replace an artificial exchange rate with the real one.

In any event, the move had massive implications. With the value of the Yuan much lower, Chinese exports became significantly cheaper than those of its competitors. By 2018, China was the world’s top trader, exporting more goods than any other country on Earth.

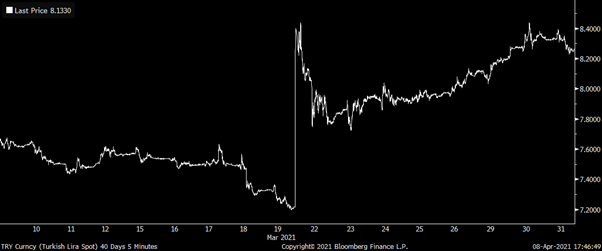

9. You’re fired! A political sacking sinks the Turkish Lira

As bad as Brexit. That’s what one expert called Turkish Prime Minister Recep Tayyip Erdogan’s decision to fire the head of the Turkish Central Bank Naci Agbal in March 2021. The Turkish Lira has been in trouble since 2018, mainly due to political interference.

Inflation — the rate at which the cost of living increases — is high. But Erdogan has prohibited the central bank from taking steps which could bring it down because he has his own ideas. (Most respected economists disagree with Erdogan. But what do they know, eh?).

Political instability has also made Turkey less attractive to investors. Less investment means less demand for the Lira, which has also negatively affected its value. Agbal, who was appointed in late 2020, briefly managed to turn the Lira’s fortunes around. But despite achieving very positive results in a mere few months, Erdogan insisted his approach wasn’t the way to go. So he promptly replaced him with Sahap Kavcioglu, a member of his political party who — to no-one’s surprise — also happens to share his views.

The saddest part is that, under Agbal’s stewardship, the Lira briefly became the best-performing emerging market currency of 2021. Unfortunately, his firing instantly slashed its value by 15% and undid Agbal’s good work.

Step off the rollercoaster

There’s an infinite number of factors that can impact exchange rates and hit your business where it really hurts.

But you know what? You don’t have to take it on the chin.

By using hedging instruments like options and currency fowards, you can lock in a favourable exchange rate and protect your business come Erdogan or high oil.

So how can hedging instruments limit your FX exposure? Well, if you want the answer, you’ll have to stay tuned. Watch this space for the next piece in the series, in which we reveal how hedging took a beloved snack from financially unfeasible to worldwide sensation.