A ratio forward is a type of structured, or ‘exotic’ option. Exotic options are derivative contracts in which two or more options are combined to create a more complex arrangement. For instance, two simple – or ‘vanilla’ options – could be combined into what would be known as a Vanilla Ratio Forward.

Despite its name, a ratio forward is more like an option than a forward. Where standard forwards always create a legal obligation to buy or sell, in a ratio forward the obligation only arises if a certain threshold is reached.

Even when the threshold is reached, a ratio forward may be structured in a way that allows you to still take advantage of market movements in your favour. But only up to a certain limit.

Imagine you’re a UK business that owes a French supplier €5,000. The money is due in December 2021.

Because of the way the economy is going, you’re concerned that, by the time the payment is due, the EUR/GBP exchange rate will make your bill more expensive. So you decide to hedge.

One option is to use a forward contract.

Here, you’d agree to buy €5,000 for a specific exchange rate. The problem is that forwards are legally binding. So if it turns out you’ve been too pessimistic and the EUR/GBP exchange rate moves in your favour, you’ll still have to make the trade. Even if the market exchange rate is much better than the rate in the forward contract.

The alternative is to buy an option. This gives you the right — but not the obligation — to buy €5,000 at a specific exchange rate.

The advantage of an option is that, if the market exchange rate is better than the rate in the option, you can ignore the option. The catch is that you have to pay a premium to buy the option. And if you end up not using the option, you’ve paid the premium for nothing.

But there’s a third alternative: a ratio forward.

Like a standard forward, a ratio forward is an agreement to buy EUR5,000 at a specific exchange rate. However, it moves the buyer beyond a binary situation. Instead, more than one option is included in the trade to do just that – provide additional options.

Effectively, what a buyer does is cover the downside risk, locking in a ‘worst case rate’. For our purposes, let’s assume the worst case rate is 1.12 GBP/EUR. The buyer agrees to buy EUR5,000 at this price, if the rate drops below this rate (to say 1.05). In this case, the buyer would have saved themselves GBP300. However, at the same time, the client places another contract to buy a larger amount of EUR (let’s say EUR5,500) if the rate moves above 1.12, to say 1.2. In this case, the client spends GBP190 extra but gets a further EUR500 vs the worst case scenario. This is a Vanilla Forward Ratio, since it involves two vanilla options.

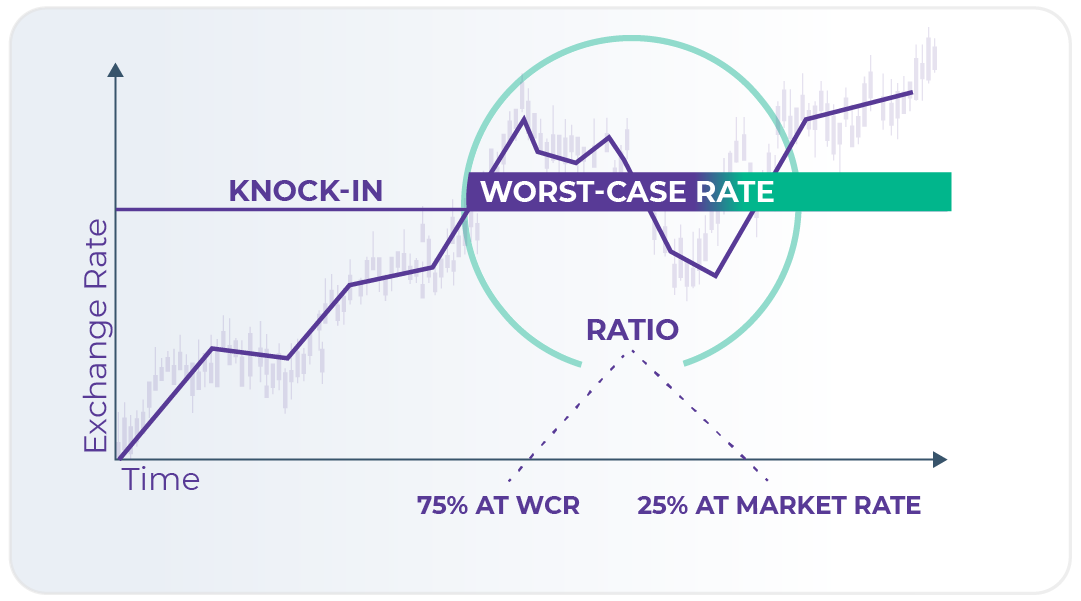

An extra step, known as a Ratio Forward Extra, would introduce another option to the scenario. Effectively, rather than setting a single strike price, the buyer can introduce a threshold or ‘barrier’. In this case, you’re only legally obliged to go ahead with the trade if the market exchange rate reaches this threshold.

And even if the barrier is reached, you don’t have to go ahead with the whole trade. There’s a percentage — or ratio — which you can buy at the market exchange rate.

Let’s say the barrier in your ratio forward is EUR/GBP 1.20 and the worst case rate is EUR/GBP is 1.17. You’ve also agreed on a ratio of 75%-25%. Which means you’re only legally obliged to buy 75% of your Euro at the worst case rate.

Three things can happen:

- In December, the EUR/GBP market exchange rate is 1.14 — better than the rate in your ratio forward and lower than the 1.20 barrier. So you buy your Euro at the market rate.

- In December, the EUR/GBP market exchange rate is 1.19. This is lower than the 1.20 barrier but higher than the worst protected rate in your ratio forward. So you use the forward to buy your Euro to get a better deal.

- At any point before December, the EUR/GBP market exchange rate hits 1.21. Because it’s over the barrier, you’re legally obliged to buy your Euro at the worst protected rate.

But because this is a ratio forward, you only have to buy 75% — that is, €3,750 — at the worst protected rate. If at any time before December the exchange rate goes back under 1.17, you can buy the remaining 25% — €1,250 — at the market exchange rate.

This type of arrangement has two benefits:

- You don’t have to pay a premium, so you can protect yourself without upfront costs.

- It’s more flexible than a forward — the legal obligation to buy only kicks in when you hit the barrier. And, even then, you don’t have to exchange everything at the worst case rate if the market turns around

The flipside is that the worst case rate won’t be as good as the rate you’d get on a standard forward contract or option. This is the price you pay for flexibility, and makes up for the lack of an upfront premium.

Some Facts

- The term ‘exotic option’ first appeared in a 1992 paper by economist Mark Rubinstein.

- It’s been suggested that Rubinstein borrowed the term from horse racing. Where novices tend to place ‘straight bets’ — bets on which horse will win, or where a horse will place — seasoned gamblers use advanced tactics like the ‘trifecta’. In a trifecta, the gambler bets on which horses will place first, second, and third. These types of wagers are known as ‘exotic bets’.

- Rubinstein himself has acknowledged this as a possibility. Before researching exotic options, he researched betting techniques that resulted in guaranteed profits. He reasons that the term ‘exotic’ might’ve stuck in this mind

Want to know more?

- This paper discusses the different types of barrier options — options that only kick in when a threshold is reached — and when you’d use them, including the different types of barriers you can have in place.

- Yes, there is such a thing as a sure bet on the horse-racing track. And a man called Bill Benter designed an algorithm that ensured he’d never lose. This is his story.

ALT21’s perspective:

“If you’re worried about exchange rate fluctuations, but would still like some flexibility in case the market goes your way (and don’t want to pay a premium), ratio forwards can be a good compromise. They’re rather complex instruments though, so make sure you understand their pros and cons before you commit.”